Address

304 North Cardinal St.

Dorchester Center, MA 02124

Work Hours

Monday to Friday: 7AM - 7PM

Weekend: 10AM - 5PM

Address

304 North Cardinal St.

Dorchester Center, MA 02124

Work Hours

Monday to Friday: 7AM - 7PM

Weekend: 10AM - 5PM

[Start W-8IMY p.1 rev.2006]

W-8IMY rev.2006 is what CW is using, however, the 2024 version is very different.

[End W-8IMY p.1 rev.2006]

Welcome, you all, to this Saturday, December 12 edition of Money Banking and Trust. I’m your host Christian Walters and we’ll continue on where we left off last week we were going over the forms the IRS Form W-8BEN. And we didn’t get a chance to get into the W-8IMY and that’s where I pick up today. So I gave you the download links for that form and the instructions for the requester of forms W-8BEN and the W-8IMY also. I would have those two forms ready.

We’re gonna go over the W-8IMY right now. Then I will open up for some questions. But this W-8IMY, just a cursory view of the form itself before you jump into the instructions.

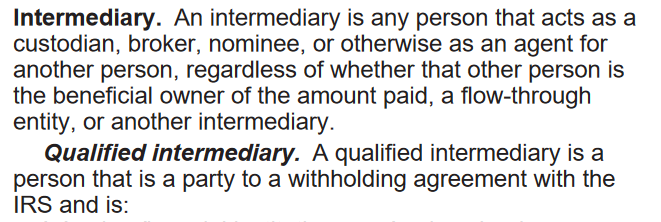

So this form is stating that it’s a certification of foreign intermediary, foreign flow through entity, or certain US branches for United States tax withholding. And on the left side gives the name of the document W-8IMY. And then something very interesting, which I brought up last week, again, which I’ll bring out again, is right below that it says “Department of the Treasury Internal Revenue Service.”

This part of Rev.2021 is substantially the same as Rev.2006

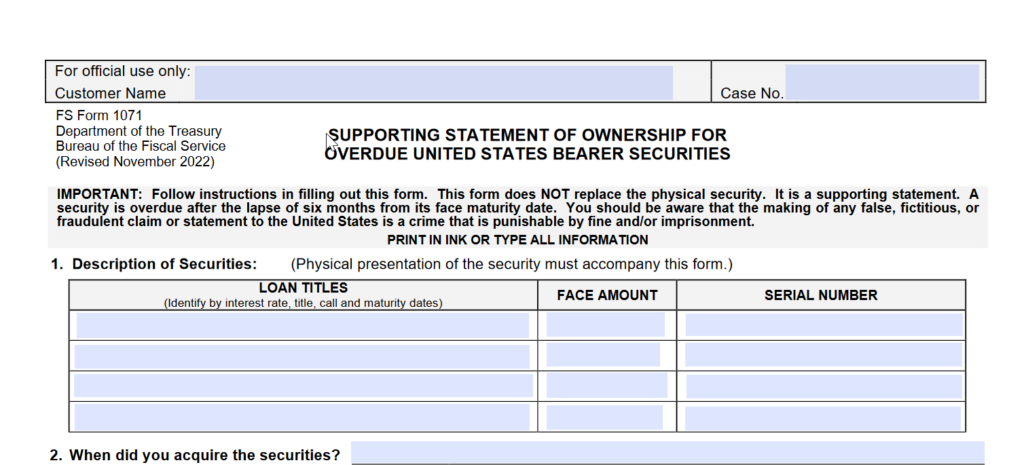

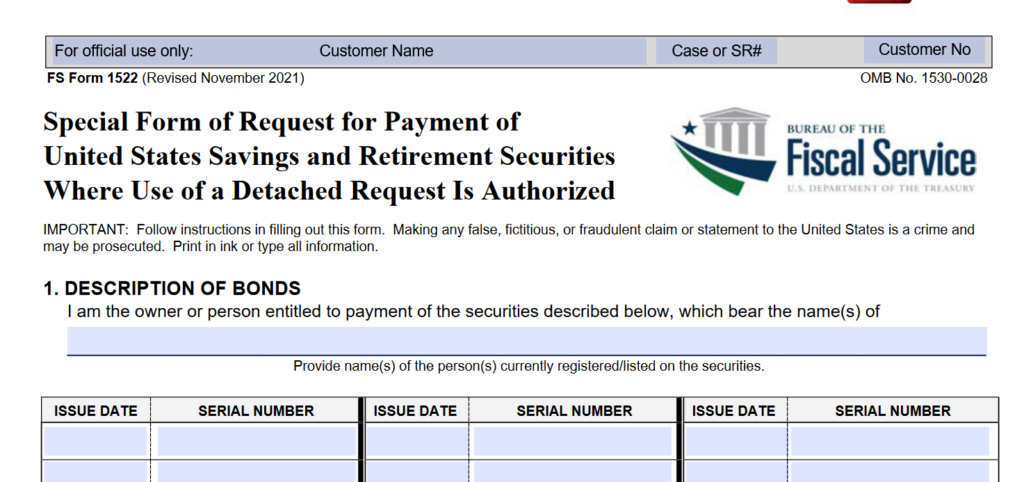

Now, some of these other documents, like the 1071, 1522, and others, if you’ll notice, on the left hand side, those documents say a little bit different.

|  |

| FS Form 1071 – Department of the Treasury – Bureau of the Fiscal Service – (Rev. Nov.2022) | FS Form 1522 – Department of the Treasury – Bureau of the Fiscal Service – (Rev.Nov.2021) |

They say, the “Department of the Treasury, Bureau of Public Debt [In 2024 it’s called The Bureau of Fiscal Services]”. I think that’s pretty significant. I think that separates the documentation of which documents are operating on public versus private. Because I think the W-8IMY along with the W-BEN doesn’t have that “Department of Public Debt [Bureau of Fiscal Services]” on there. So the Department of Public Debt [Bureau of Fiscal Services] is really the public side. And the the other one doesn’t state that on there, the W-8IMY and the W-8BEN, doesn’t have it on there. And those documents, I believe, are on the private side. So I would, you know, pay particular attention to the details in some of the wording that they use. Especially Black’s Law. Don’t assume that anything that they’re they’re talking about in there that you understand the terms that they’re using in any of this documentation, because it’s really all legal speak and unless you have a Black’s Law or some kind of legal dictionary looking at these terms, could mean something totally different.

So basically the form is talking about a certification of the entity or the intermediary, the US branch or the partnership or the trust. And the purpose of the form is really stating the certification of your status. The certification of your status. And that was also basically the W-8BEN, also.

And the next block down it says:

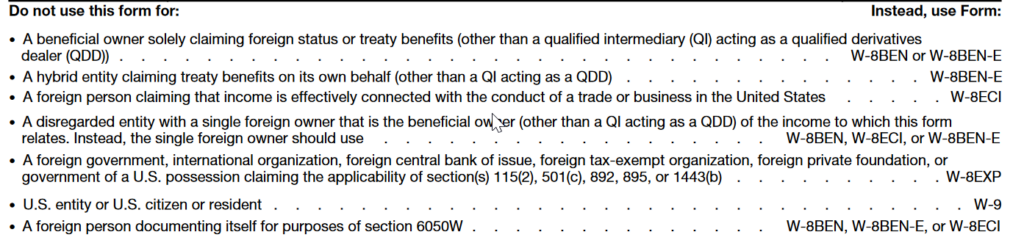

“Do not use this form if:” for whatever reason and they give you five bullets there and then it says to the right, “Instead use these forms,” and they’re referencing you to the W-8BEN. On some of these, and the W-8ECI when ECI means effectively connected income to a US trade or business.

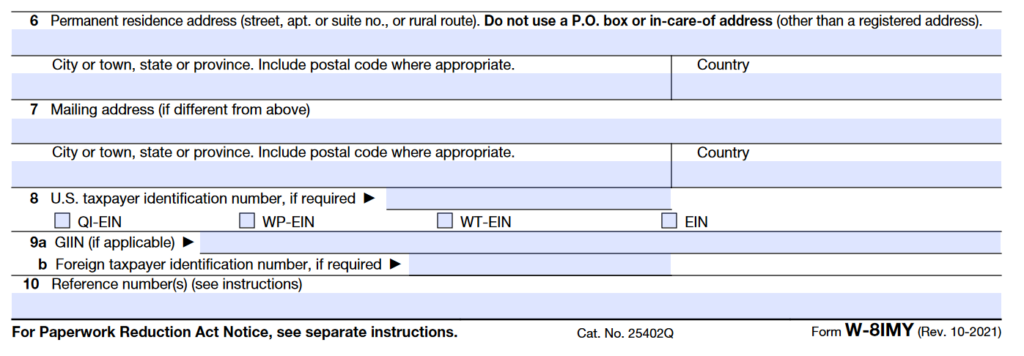

So, the next, part one, is the identification of the entity.

[Start rev.2006]

[End rev.2006]

[Start rev.2021]

[and skip to bottom:]

[End rev.2021]

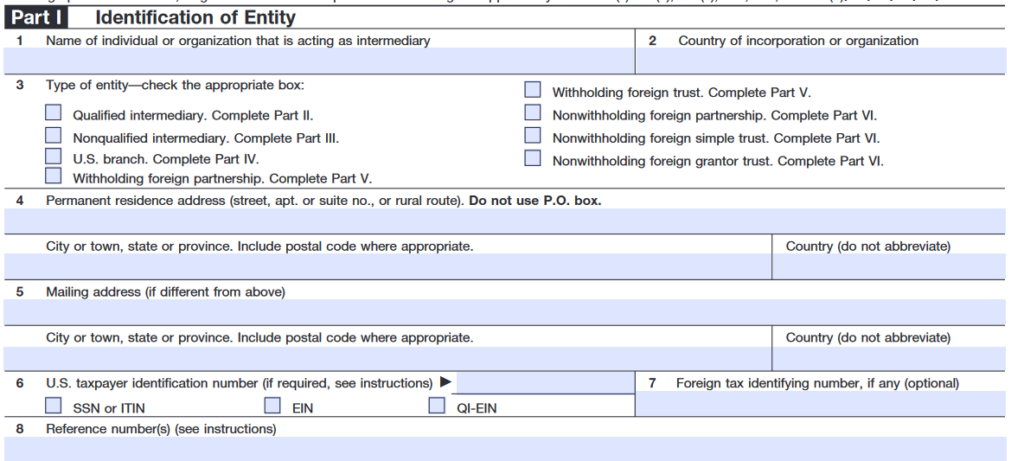

And it lists the, the individual and block one or the organization that is acting as intermediary. So it’s one or the other.

And then three [#4 in rev.2021]:

[Start rev.2006 p.1]

[End rev.2006]

[Start rev.2021 #4 p.1 “Chapter 3 Status (entity type)”]

[End rev.2021]

Block three is a type of entity. And you’d have to check one of those blocks to describe your status. So, which one you are.

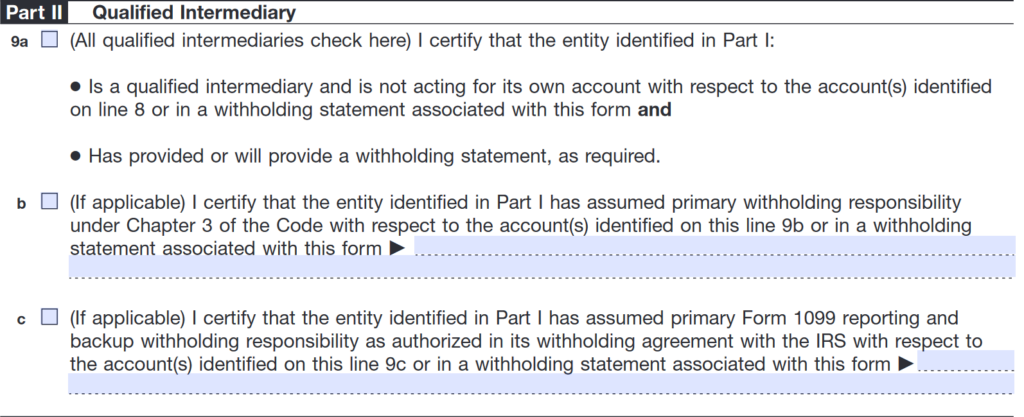

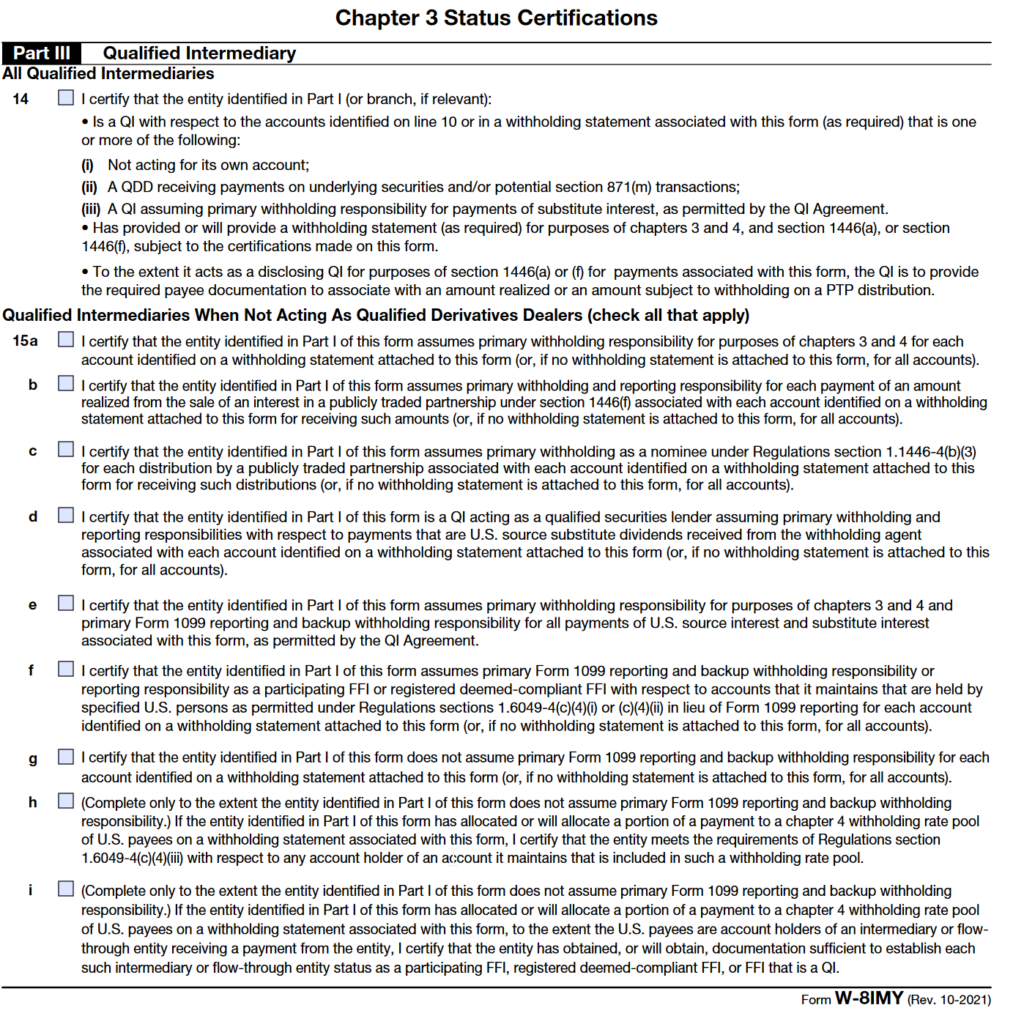

And Part two then, “Qualified Intermediary.”

[Start rev.2006]

[End rev.2006]

[Start rev.2021 p.2 part.3 to p.3 ]

[End rev.2021]

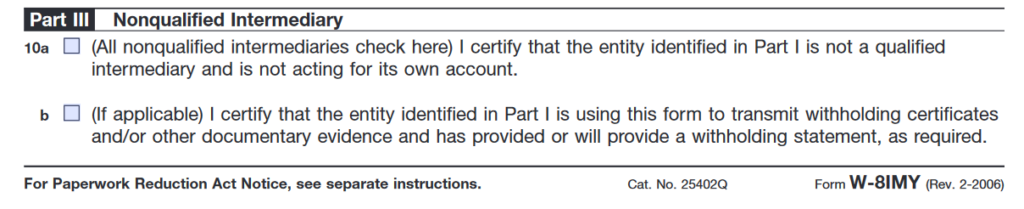

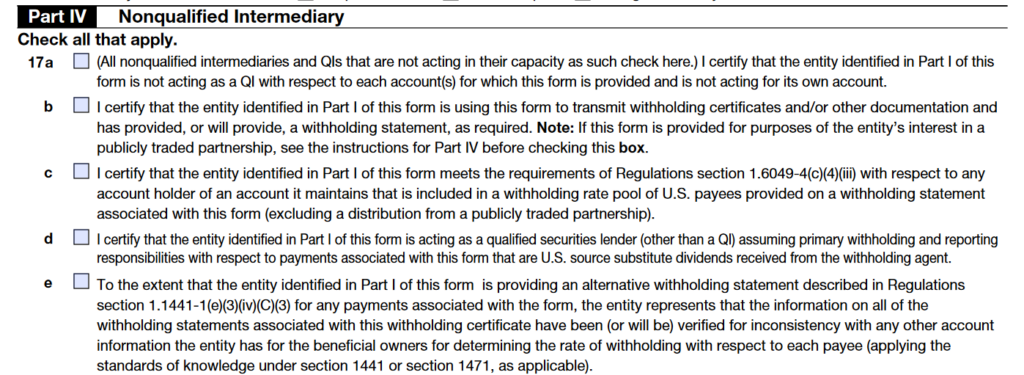

Part three is Nonqualified Intermediary.

[Start rev.2006]

[End rev.2006]

[Start rev.2021 p.3 part.4 17a-d]

[End rev.2021]

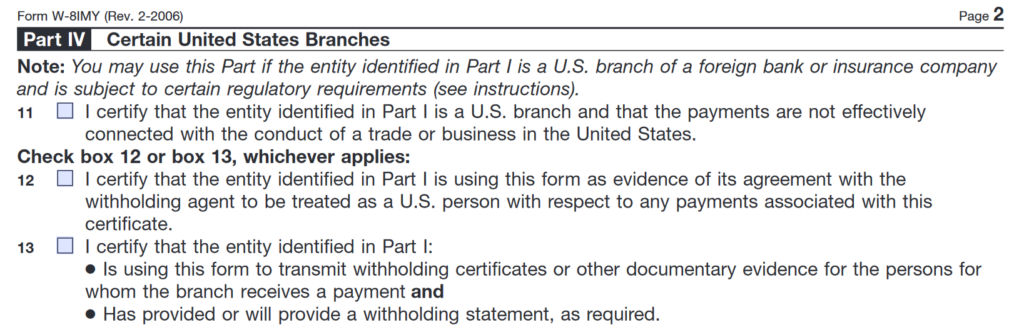

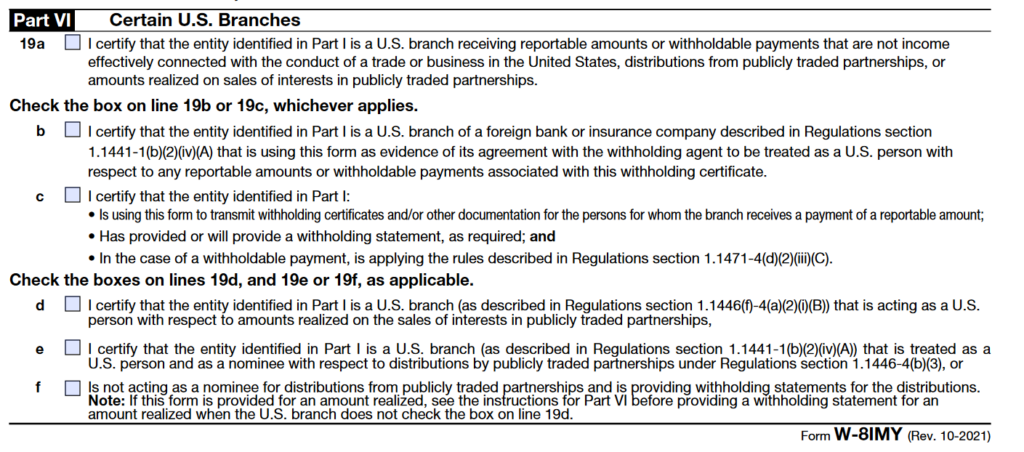

And the next page is part four, talking about certain US branches.

[Start rev.2006]

[End rev.2006]

[Start rev.2021 p.3 part.6]

[End rev.2021]

And part five which is withholding foreign partnership or withholding foreign trust.

[Start rev.2006]

[End rev.2006]

[Start rev.2021 p.4 part.7]

[End rev.2021]

Now, notice those are withholders.

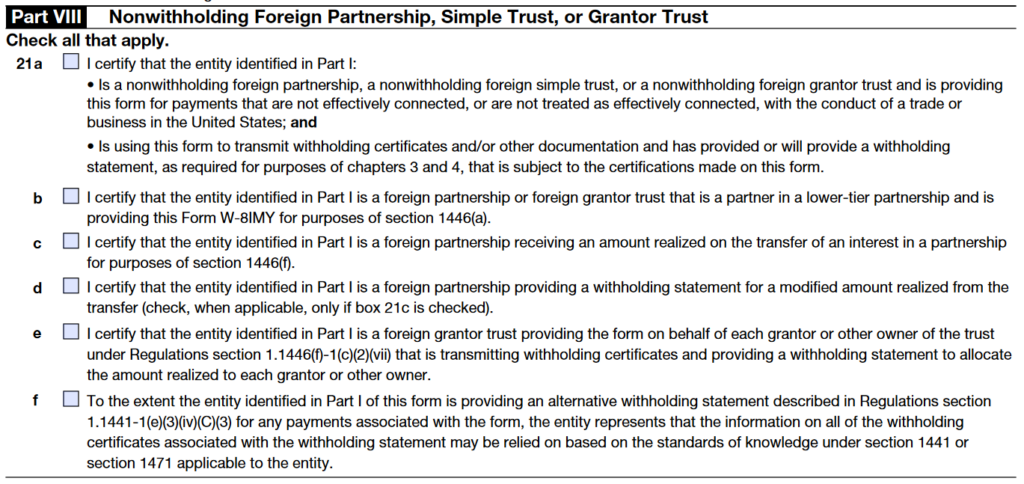

And part six, which is non withholding, foreign partnership, simple trust or grantor trust.

[Start rev.2006]

[End rev.2006]

[Start rev.2021 p.4 part.6 #21a-f]

[End rev.2021]

So that’s the non withholding section.

And you’re certifying that in part six.

[Start rev.2006]

[End rev.2006]

[Start rev.2021 p.4 part.8 #21a]

[End rev.2021]

“That the entity identified in part one and the two bullets there is that is a non withholding foreign partnership or non withholding foreign simple trust or a non withholding foreign grantor trust and that the payments to which this certificate relates are not effectively connected or do not or are not treated as effectively connected with the conduct of a trade or business in the United States; and” next bullet “Is using this form to transmit withholding certificates and or other documentary evidence and has provided or will provide it withholding statement as required….”

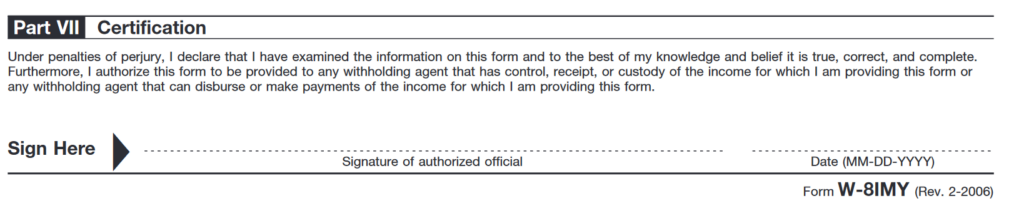

And the next part seven there, the certification.

[Start rev.2006]

[End rev.2006]

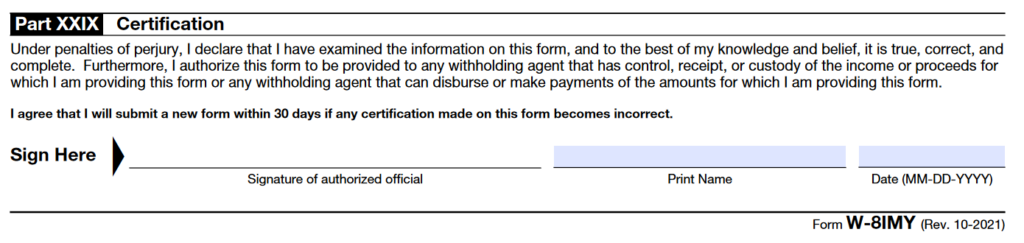

[Start rev.2021 p.8 part.29]

[End rev.2021]

So notice that this is a declaration, it’s not a sworn-to statement, it’s a declaration. So, “Under penalties of perjury, I declare that–” blah, blah, blah. And it says next line, “Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income for which I am proving providing this form or any withholding agent that has that can disperse or make payments of the income for which I’m providing this form.” So the disbursements and the payment of the income, the certification of that.

So now we’ll jump to the the instructions section here.

[Start rev.2006]

[End rev.2006]

[Start rev.2021 Definitions are on page 4]

[End rev.2024]

So page one of the instructions, the general instructions. So it says that under the note there, “For the definitions of terms used throughout these instructions, see definitions on page two and three.” And that’d be the first thing I would jump to on their definitions to find out, you know, what these terminologies are. And then I would check up the words out of Black’s Law or some legal dictionary to find out what those terms in those definitions really are.

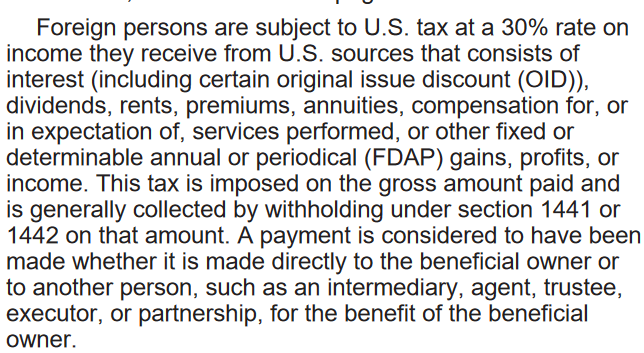

So, “Foreign persons are subject to US tax … on income they receive from US sources, and that consists of interest and that interest including certain , original issue discounts, (OID) dividends, rents, premiums, annuities, compensation for or an expectation of services performed, or other fixed determinable annual or periodical … gains, profits or income. This tax was imposed on the gross amount paid and is generally collected by withholding under sections 1441 or 1442 on that amount. A payment is considered to have been made whether it was made directly to the beneficial owner or to another person such as an intermediary agent, trustee, executor or partnership for the benefit of the beneficial owner.”

So “Foreign persons are also subject to tax at graduated rates on income they earn that is considered effectively connected with a US trade or business.” Well, think about the opposite of that! [Foreign persons are not subject to tax on income they earn that is not effectively connected with a US trade or business.]

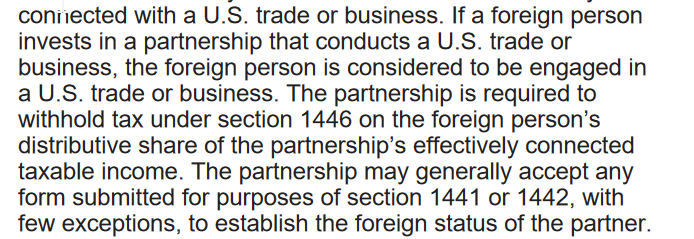

So “If a foreign person invests in a partnership that conducts a US trade or business, the foreign person is considered to be engaged in the US trade or business. And the partnership is required to withhold tax under Section 1446 on foreign persons distributive share of the partnerships effective connected taxable income, the partnership may generally accept any form submitted for purpose of section 1441 or 1442 With few exceptions to establish the foreign status–” And remember I said that this whole form is talking about status, certification of status. So “–to establish the foreign status of the partner –“and it goes on talking about the regulations there.

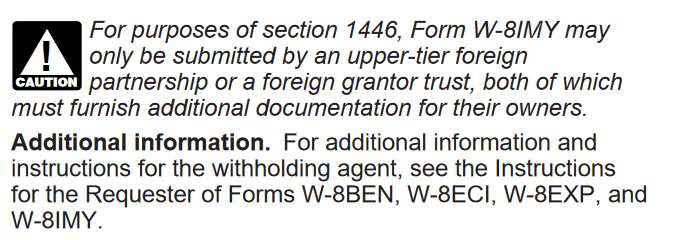

But then the caution it says that, “For purposes of section 1446, form W-8IMY may be submitted by an upper tier foreign partnership or foreign grantor trust, both of which must furnish additional documentation for their owners.” And that goes into the additional information for the “Additional information the instructions for withholding agent see Instructions for the Requester of Forms W-8BEN and W-8IMY–” which we went over a little bit on last week’s program page, I think it was six and seven, which was really talking about there and that for a substitute W-8BEN or a substitute W-8IMY you don’t really have to use these forms.

So “Who must file Form W-8IMY.” The bullet says that “A foreign person or a foreign branch of a US person to establish that is a Qualified Intermediary that is not acting for its own account.” I’m gonna skip to the next one.

Next bullet here is “A foreign person to establish that as a nonqualified intermediary–” So it’s running down through the the options here “–that is not acting for its own account and if applicable, that it is using the forms to transmit withholding certificates.”

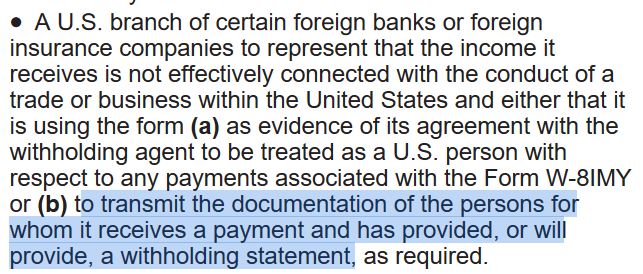

And the next one is a US branch and I didn’t see too much really in there other than was withholding statements.

And the next bullet is foreign partnerships,

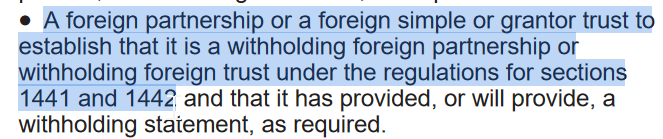

which would be “A foreign partnership or a foreign simple or grantor trust to establish that it is a withholding foreign partnership or withholding foreign trust under the regulations for sections 1441 and 1442.” So it is a withholder, there.

And the next bullet:

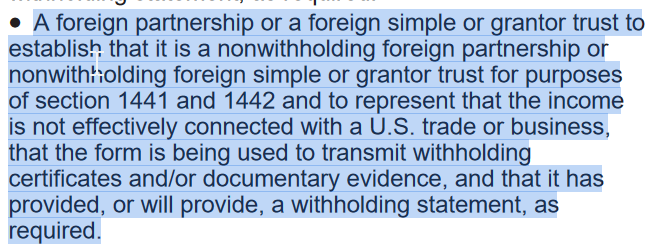

“A foreign partnership or foreign simple trust or grantor trust to establish that it is nonwithholding foreign partnership or nonwithholding foreign simple trust or grantor trust for the purpose of section 1441 and 42. And to represent that the income is not effectively connected with the US trade or business and that the form is being used to transmit withholding certificates and our documentary evidence and that is provided or will provide a withholding statement as required.”

So that section is pretty important. Next section I didn’t see too much in that. Next paragraph with the next bullet:

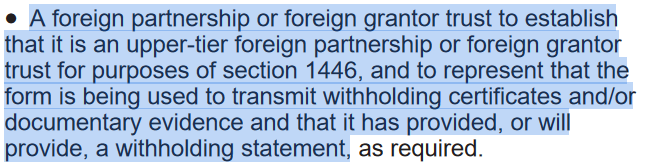

“Foreign partnership or foreign grantor trust to establish that is an upper tier of foreign partnership or foreign grantor trust for purposes of section 1446. And to represent that the form is being used to transmit withholding certificates and or documentary evidence and it is provided a will provide and withholding statement as required.”

We’re still on page one here at the bottom right hand column here we’re on the last bullet:

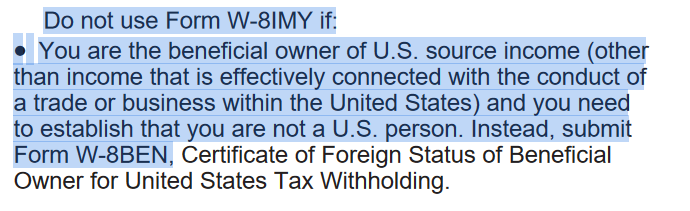

“Do not use form W-8IMY if you’re a beneficial owner of U.S. source income (other than income and effectively connected with the conduct of a trade or business within the United States) and you need to establish that you are not a U.S. person. Instead submit Form W-8BEN, Certificate of Foreign Status of Beneficial Owner for United States withholding.”

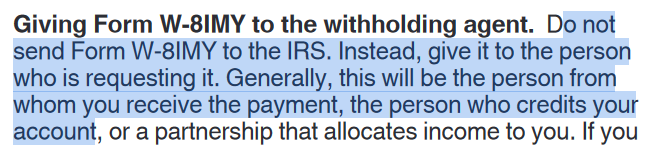

Okay next page, page two. I didn’t really see a whole lot till about three quarters of the way down that first column where it was talking about giving form W-8IMY to the withholding agent.

It says, “Do not send Form W-8IMY to the IRS. Instead give it to the person who is requesting it. Generally this person will be the one from whom you receive the payment who credits your account.”

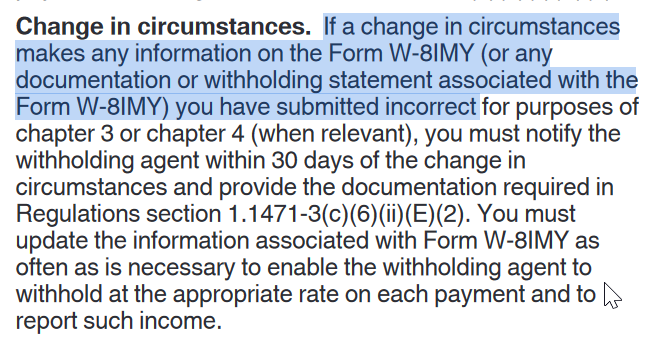

And the next paragraph then is the changes in circumstances:

It says, “If a change in circumstances makes any information on the Form W-8IMY … you have have submitted incorrect … you must notify the witholding agent–” or, the payer “– within 30 days … and …” then you must file a new form W-8IMY to provide new documentation or new withholding statement.” Then, think of this document, or really all these documents, as really like fiction-form material. And the only thing that’s really showing up on them is really a fiction.

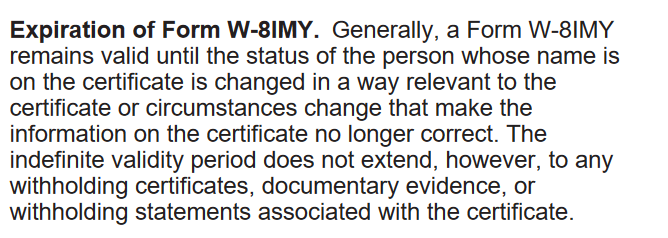

Next column then the top: Expiration of Form W-8IMY.

So, “Generally, a form W-8IMY remains valid until the status of the person whose name is on the certificate is changed in a way relevant to the certificate or circumstances change that make the information on the certificate no longer correct. The indefinite validity period does not extend, however, to any withholding certificates, documentary evidence, or withholding statements associated with the certificate.”

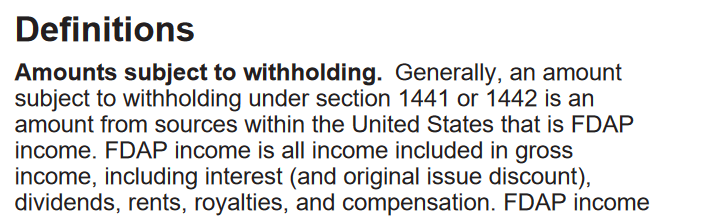

So now we come into the definitions there, which probably should have been the first thing we’ve probably read but anyway. “The amount subject to withholding.” That’s pretty much self-explanatory because we went over that last week and they’re about the same there.

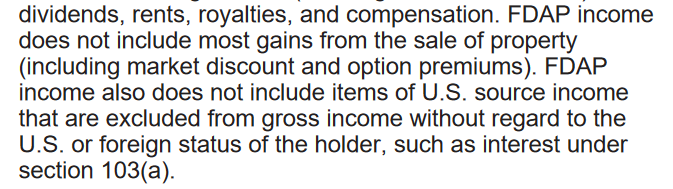

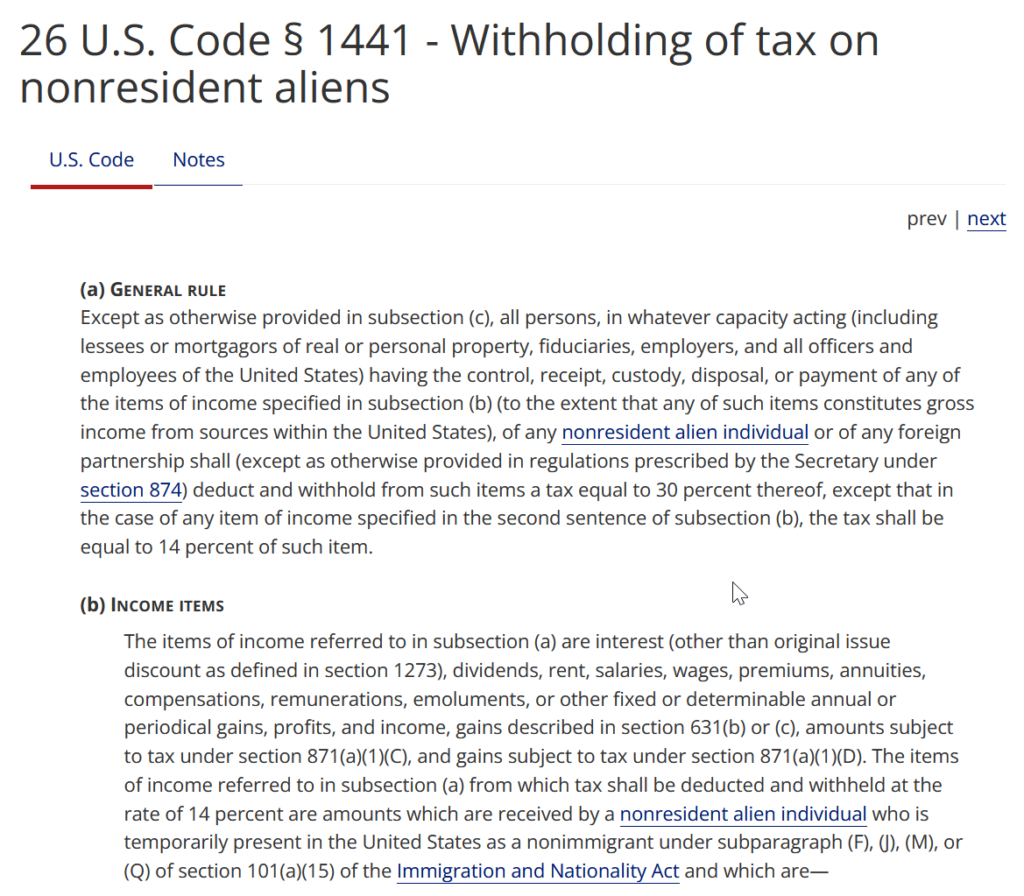

“Amounts subject to withholding. Generally, an amount subject to withholding under section 1441 or 1442 is an amount from sources within the United States that is FDAP income. FDAP income is all income included in gross income, including interest (and original issue discount), dividends, rents, royalties, and compensation.

Talking about “Interests” and the “OID,” I would check that out a little further.

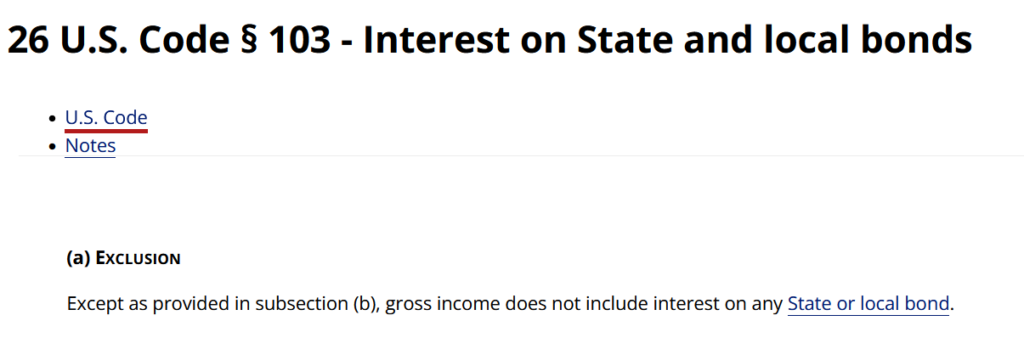

“FDAP income does not include most gains from the sale of property (including market discount and option premiums). FDAP income also does not include items of U.S. source income that are excluded from gross income without regard to the U.S. or foreign status of the holder, such as interest under section 103(a).

And I would check out that section under interest.

Next paragraph says:

“Generally an amount subject to withholding under Section 1446 is an amount that is or is treated as effectively connected income of a US trade or business of the partnership.”

Now coming into the definition of beneficial owner. And I didn’t know if that was clear from when I did that definition on the W-8BEN there, but I’ll try and maybe do a little bit better. I felt like I didn’t quite get it across the way I wanted to say it, but:

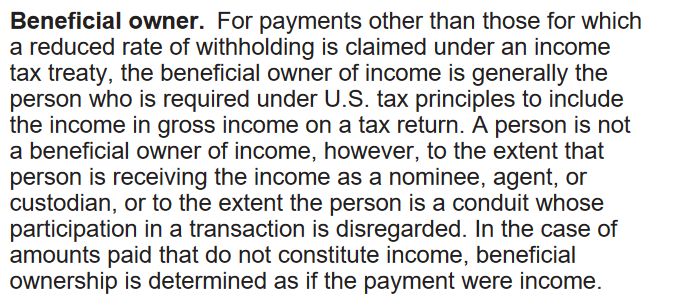

“Beneficial owner. For payments other than those which a reduced rate of withholding is claimed under an income tax treaty, the beneficial owner of income is generally”–generally–“the person who is required under US tax principles to include the income and gross income on a tax return. A person is not the beneficial owner of income, however, to the extent that the person is receiving the income as a nominee, an agent, or custodian, or to the extent the person is a conduit, whose participation in a transaction is disregarded. And in a case of amounts paid that do not constitute income, beneficial ownership is determined as if the payment were income.” So these terms that you’re not sure what the meanings are, I would definitely look them up, especially these key words that I’ve given you some emphasis to. You can look them up in Black’s Law.

“GENERAL. From Latin word genus. It relates to the whole kind, class, or order. … Pertaining to or designating the genus or class, as distinguished from that which characterizes the species or individual; universal, not particularized, as opposed to special…“

And now the next paragraph:

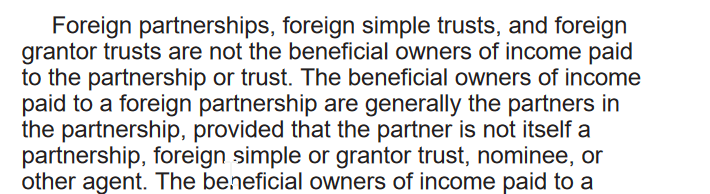

“Foreign partnerships, foreign simple trusts and foreign grantor trusts are not the beneficial owners of income paid to the partnership or trust. The beneficial owners of the income paid to the foreign partnership are generally the partners in the partnership, provided that the partner is not itself a partnership, foreign simple trust or grantor trust nominee or other agent.”

So I’ll back up a little bit here, this foreign partnership, I classified that last week as the Number One, I believe. And the Number Two then would be the foreign simple trust. And Number Three would be the foreign grantor trust. And then on the W-8BEN of last week, there was a Fourth one, which was the foreign complex trust. And I don’t believe they talked about that in here, but I think it is it’s at the bottom same way. I see it down there.

Alright, so the foreign simple trusts and foreign grantor trusts, they’re not the beneficial owners of income paid to the partnership or trust. The beneficial owners of the income paid to a foreign partnership are generally the partners. So there’s your beneficial owners in a partnership there is Number One, that’s the partners.

And skipping down a little bit:

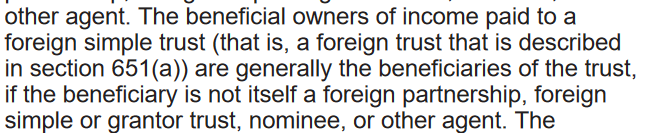

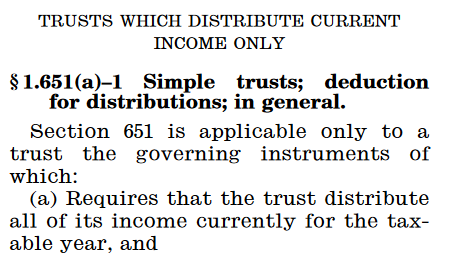

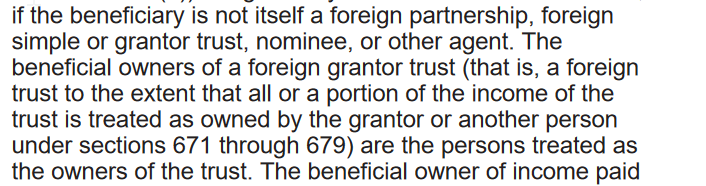

“The beneficial owners of the income paid to a foreign simple trust (that is, a foreign trust that is described in Section 651(a)) are generally the beneficiaries of the trust…”

So, the beneficial owners in foreign simple trusts are the beneficiaries.

“…If the beneficiary is not itself a foreign partnership, foreign simple or grantor trust, nominee, or other agent. The beneficial owners of a foreign grantor trust (that is, a foreign trust to the extent that all or a portion of the income of the trust is treated as owned by the grantor or another person under sections 671 through 679) are the persons treated as the owners of the trust.” So the beneficial owners of a foreign simple trust are the beneficiaries of the trust. And the foreign grantor trusts is going to be the grantor is the owner.

And then the last one:

“The beneficial owner of income paid to a foreign complex trust (that is, a foreign trust that is not a foreign simple trust or foreign grantor trust) is the trust itself.” I think they’re using the modern view because the modern view is that the trust itself can be the owner, but on the older view would have to be that the trust would have to be the trustees. The trustees would be the owner in a foreign complex trust. So the beneficial owner of income paid to foreign estate is the estate itself.

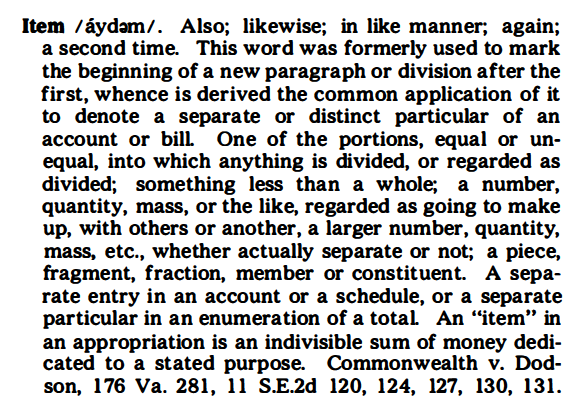

Then we start the fiscally transparent entity. So “…with respect to an item–“And make sure that you look up the word “item,” because there are non cash items and there are cash items. Non-cash items are non-negotiable. Cash items are negotiable. Nonnegotiable means private. Negotiable means public.

Item. … A separate entry in an account or a schedule, or a separate particular in an enumeration of a total. An “item” in an appropriation is an indivisible sum of money dedicated to a stated purpose… Any instrument for the payment of money, though not negotiable, but not money. U.C.C. sec.4-104(1)g

— Black’s Law 5th Ed.

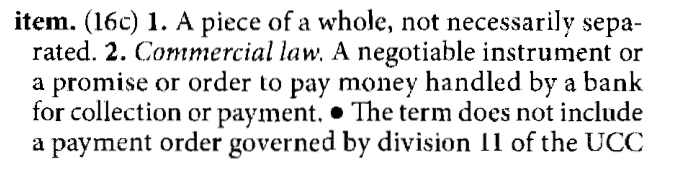

item. … Commercial law. A negotiable instrument or a promise or order to pay money handled by a bank for collection or payment. … does not include a credit- or debit-card slip.

Black’s Law 9th Ed. (2009)

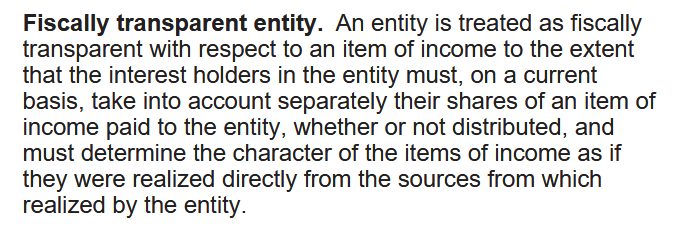

“A fiscally transparent entity with respect to an item of income…” (I’m gonna skip a little bit interest holders and the entity) “…must … take into account separately their shares of an item of income paid to the entity … and must determine the character of the items–” Must determine the character of the items “–of income as if they were realized directly from the sources from which is realized by the entity.” So the sources they want to see whether or not it’s an ECI, which is effectively connected income to a US business or trade. So, its importance is to find out or identify the source.

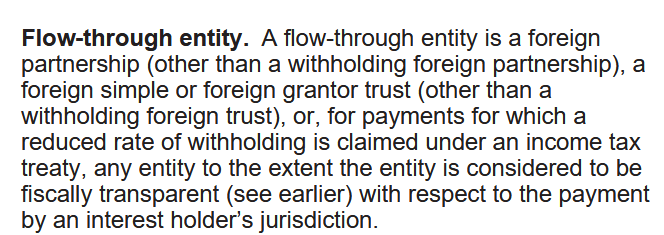

“Flow-through entity. A flow-through entity is a foreign partnership (other than a withholding foreign partnership), a foreign simple or foreign grantor trust (other than a withholding foreign trust), or, for payments for which a reduced rate of withholding is claimed under an income tax treaty, any entity to the extent the entity is considered to be fiscally transparent (see earlier) with respect to the payment by an interest holder’s jurisdiction.”

“Foreign person. A foreign person includes a nonresident alien–” a foreign person includes a nonresident alien “–individual, a foreign corporation, a foreign partnership, a foreign trust, a foreign estate, and any other person that is not a U.S. person.” Sounds good to me!

“It also includes a foreign branch or office of a U.S. financial institution or U.S. clearing organization if the foreign branch is a qualified intermediary. Generally, a payment to a U.S. branch of a foreign person is a payment to a foreign person.”

They go into a hybrid entity. And I think I’ll skip that.

And then qualified intermediary.

“A Qualified Intermediary is a person that is a party to a withholding agreement.” An example would be, say an employer, because an employer agrees with the IRS and now they are a partner with them, and they’re a partnership. And they now have an agreement to withhold so they’re now a Qualified Intermediary.

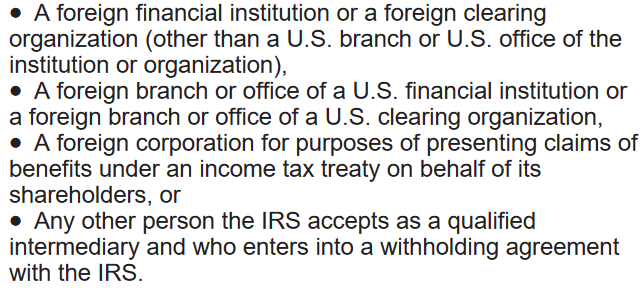

So “…a party to a withholding agreement with the IRS and is a foreign financial institution or foreign Clearing Corporation.” Next one is “A foreign branch or office of a US financial institution.” And the next one, “A foreign corporation for purpose of presenting claims of benefits under an income tax treaty on behalf of its shareholders.” And the next one: “Any other person the IRS accepts as a Qualified Intermediary, and who enters into a withholding agreement with the IRS.” And that could be just as easy as commingling your funds in the public from the private. And then we wonder why we have so much problems under debtor-creditor law!

Now, a nonqualified intermediary.

“A nonqualified intermediary is an intermediary that is not a US person that is not a qualified intermediary.”

And a nonwithholding foreign partnership or simple trust or grantor trust:

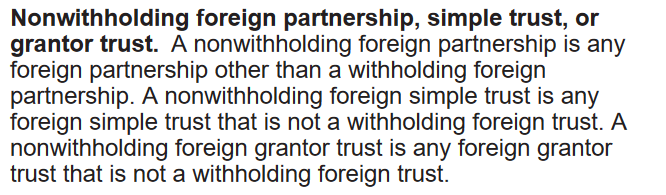

“A nonwithholding foreign partnership is any foreign partnership other than a withholding foreign partnership. A nonwithholding foreign simple trust is any foreign simple trust that is not a withholding foreign trust. A nonwithholding foreign grantor trust is any foreign grantor trust that is not a withholding foreign trust.”

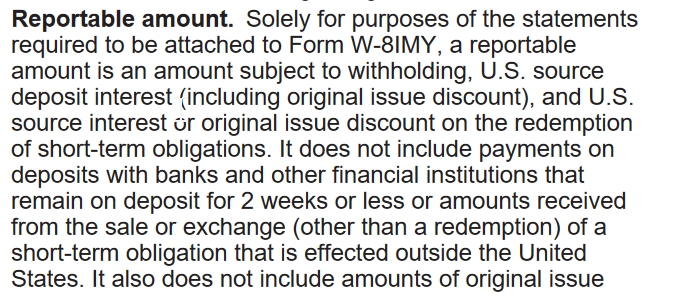

“Reportable amount. Solely for purposes of the statements required to be attached to Form W-8IMY, a reportable amount is an amount subject to withholding, U.S. source deposit interest (including original issue discount–“OID! “–), and U.S. source interest or original issue discounts–“OIDs “–on the redemption of short-term obligations. It does not include payments on deposits with banks and other financial institutions that remain on deposit for 2 weeks or less or amounts received from the sale or exchange (other than a redemption) of a short-term obligation that is effected outside the United States.“

So it does not include payments on deposits with banks and other financial institutions or amounts received from the sale or exchange (other than redemption) of a short term obligation is affected outside the United States.

“It also does not include amounts of original issue discount arising from a sale or repurchase transaction completed within prior two weeks or less, or amounts described in regulation sections–” blah, blah, blah.

[END Christian Walters’ W-8IMY presentation]

Take NOTICE and ACKNOWLEDGEMENT with agreement that this show and/or documents is PRIVATE, and not to be construed or relied upon as being legal advice for any individual legal situation or employed for making legal decisions, and you will not use any of this information for making a legal decision or performing a legal procedure, and is not a substitute for legal advice and/or guidance by a licensed attorney. This private show and/or documents are for academic, informational purposes only to be used at your own risk, without liability to Edifie.co or its sub-trusts (“the Trust”). By accessing or reviewing this show, or using the documents therein, you understand with agreement that, with all rights reserved, without prejudice, The Trust is not an attorney licensed to practice law in the State of Florida, or any other State, and has not given legal advice, or accepted fees for legal advice, provided no assistance, advising, or guidance of any kind, for use by non-attorneys or pro se parties in the preparation or use of the therein reference, and has no interest in any issue referenced to it therein, and is not a party to this, or any action arising from, and is only acting as an authorized capacity as liaisons to communications between the parties. By reading and/or using this information you acquire knowledge, and agree that you are not a client of The Trust. These documents and show recordings are incomplete and void without this NOTICE AGREEMENT being attached herein by reference, and a breach of this agreement. Upon breach of this agreement, the breaching party becomes liable for ADMIRALTY COMMERCIAL DAMAGES of $100 million dollars per stultification or impairment per The Trust’s discretion. Thank you for your understanding.